Note: The article also got published in WE School's (Welingkar) magazine

Introduction

What is seen is often far off from reality. In the physical manifestation what is perceived is mostly in accordance with what is seen; in economics it is not so. So while an institution appears like a bank, lends like a bank & works like a bank, it is often not a bank. It is a shadow bank.

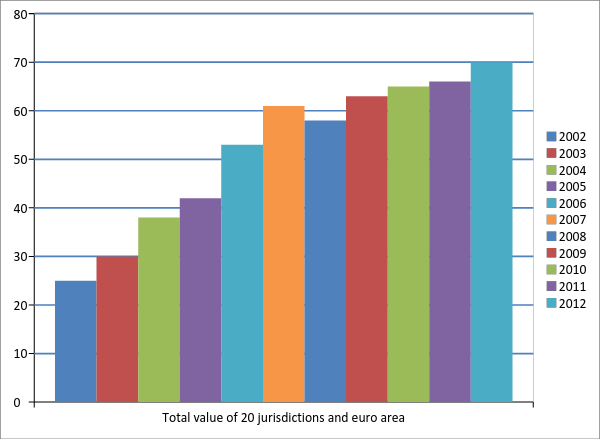

According to Financial Stability Board (FSB), a framework with representatives from the major economies of the world designed to guard against impending future crises, shadow banking is one of the most vital issues posing dangers to the global economy. Though the global size of the shadow banking market is disputed, most big shot reporting firms, including Bloomberg, peg it to be over $70 trillion! Financial Stability Board also reported this number to be $71 trillion in 2012. This is unfathomable considering that a decade ago the picture was very different. The graph below highlights the growth of shadow banking market in absolute terms over the last decade.

What is shadow banking?

Shadow banking is defined as the process of lending credit by institutions other than the regulated scheduled banks in the country. These institutions serve as intermediaries between short-term investors and long-term borrowers thus making profits from either the fees or the arbitrage in interest rates or both. Shadow banking surely has the characteristics to play a party-pooper for economies across the world. Given the vulnerabilities that this system is exposed to and the astonishing growth path it has witnessed in the last decade it has become imperative to safeguard economies against its ill-effects.

How are shadow banks different from formal banks?

Unlike a conventional bank which depends on taxpayers and savings account depositors for their sources of funds, shadow banking system relies on short term investors in the money market. Prima facie this might seem to be a perfectly dependable option to source funds, but it is not because of its dependencies on the outside market and investor’s whims and fancies.Every lending institution engages in the process of maturity transformation to lend money in the market. For example, when banks use the depositor’s short term funds to finance long term loans they engage in maturity transformation. Non-banking entities, which form the shadow banking system, do the same exercise but with a slightly different mechanism. They buy assets, say mortgages, and then bundle them into a pool to finally split and create securities out of it. These securities are then sold to the investors. This forms the major chunk of funds sourced by SB entities. The value of the security is backed by the value of the mortgage asset and the earnings on the MBS are paid from the regular interest and principal payment by the homeowners on their mortgage loans. Shadow banks have been in the fore of late especially because of their ability to securitize mortgages.

Why is shadow banking a concern around the world?

Shadow banking is touted as one of the biggest threats to the global economy. But isn’t it good enough if banking ancillary services are offered by institutions outside the banking industry? Doesn’t it create more competition among the banks and improves the quality of services as a whole?

Actually the potential point of concern here is not provision of banking facilities alone but provision of credit. If a non-banking entity, say Amazon, tomorrow comes up and helps people to manage their funds and assets, it would be welcomed rather than being questioned. The problem with shadow banking is the lending exercise they engage in. This is primarily because lending institutions are inherently fragile and play around maturity transformation to maximize profits. In this effort they tend to create enormous “maturity mismatches” and if at all there is a run on the institution they fall short of liquidity. Having said that, here is where the problem starts – traditional banking system is highly regulated by the central bank which is a watchdog to keep the banks within their safe lending limits. So, the capital adequacy of a bank is upheld. In addition to this, conventional banks are also backed by the government which acts as a safety net in case the banking system collapses. Both of the above mentioned points that help the traditional banks gain stability and credibility are elusive to the shadow banking system which is largely unregulated and not backed by any sovereign fund. This makes the SBS a trifle times more vulnerable and prone to market sentiments. SBS also got itself into bad light due to its engagement in lending using financial instruments that are called Off Balance Sheet (OBS) vehicles in financial parlance. These loans have no mention in the books of the institution which makes them very difficult to track and assess. OBS vehicles are typically considered to be separate from the banks but in practice are dependent on them.

How did the Shadow Banking System achieve its present size and avatar?

The birth of Shadow Banking system can primarily be attributed to the wariness of the scheduled commercial banks to lend money to small and medium scale businesses. The banks, beaten and battered, still coping with the bruises of the financial crisis are on the back foot and tend to retrench their expenses. Post crisis the banks have also been, rightly so, forced upon by more regulations which makes granting loans a lot more regulated activity now.

A typical supporting example is that of Republic of China. In China unlike other countries where market parameters play a vital role in setting the interest rate, it is the government that pins the interest rates for commercial lending. The government also imposes limits on loans and deposits that the banks can offer. The objective behind these regulative norms is to guarantee risk free profits for the banks. But, this leaves no incentive for the banks to remain competitive in the market by offering attractive lending rates to the customers. The result is focussed lending only to the state owned enterprises, which have near zero chances of default and are always backed by the government. Small and medium scale enterprises are thus left out of the official financial system and have no scope of borrowing money from the banks that are part of this farce system. As a result, SMEs look up to non-bank entities for credit which spawns the growth of institutions that engage in credit lending at high interest rate and take advantage of the situation. This constitutes the web of non-bank entities that make up the SBS. The Diplomat reports that China has grown to be the epicentre of ‘covert banking’ in recent times and shadow banking in China has grown by a startling 40% last year. Apparently, China is one country where shadow banking operations have grown at a rate more than formal banking operations have! JP Morgan pegs the size of the Chinese shadow banking operations to close to 46-50 trillion Yuan or $7.5-8 trillion which is about 30% of their total bank assets.

Conclusion

The authorities around the world are concerned about the shadow banking activities that have seen a manifold increase in the recent past - so much so, that shadow banking operations have affected the traditional financial sector and also the economy in general. Economists are examining more and more data closely to find the hidden vulnerabilities in this system and devise a solution for it. The most important step being taken by the authorities is to bring the area of operation of shadow banks under their purview so that the sector can be regulated and overseen thoroughly. One thing is for sure, shutting down shadow bank operations abruptly is out of question now; the way out lies in exercising greater control and expanding the scope of regulation in the financial market across all domains and sectors.

Pseudonym : h!v

Introduction

What is seen is often far off from reality. In the physical manifestation what is perceived is mostly in accordance with what is seen; in economics it is not so. So while an institution appears like a bank, lends like a bank & works like a bank, it is often not a bank. It is a shadow bank.

According to Financial Stability Board (FSB), a framework with representatives from the major economies of the world designed to guard against impending future crises, shadow banking is one of the most vital issues posing dangers to the global economy. Though the global size of the shadow banking market is disputed, most big shot reporting firms, including Bloomberg, peg it to be over $70 trillion! Financial Stability Board also reported this number to be $71 trillion in 2012. This is unfathomable considering that a decade ago the picture was very different. The graph below highlights the growth of shadow banking market in absolute terms over the last decade.

|

| Source: Financial Stability Board |

Shadow banking is defined as the process of lending credit by institutions other than the regulated scheduled banks in the country. These institutions serve as intermediaries between short-term investors and long-term borrowers thus making profits from either the fees or the arbitrage in interest rates or both. Shadow banking surely has the characteristics to play a party-pooper for economies across the world. Given the vulnerabilities that this system is exposed to and the astonishing growth path it has witnessed in the last decade it has become imperative to safeguard economies against its ill-effects.

How are shadow banks different from formal banks?

Unlike a conventional bank which depends on taxpayers and savings account depositors for their sources of funds, shadow banking system relies on short term investors in the money market. Prima facie this might seem to be a perfectly dependable option to source funds, but it is not because of its dependencies on the outside market and investor’s whims and fancies.Every lending institution engages in the process of maturity transformation to lend money in the market. For example, when banks use the depositor’s short term funds to finance long term loans they engage in maturity transformation. Non-banking entities, which form the shadow banking system, do the same exercise but with a slightly different mechanism. They buy assets, say mortgages, and then bundle them into a pool to finally split and create securities out of it. These securities are then sold to the investors. This forms the major chunk of funds sourced by SB entities. The value of the security is backed by the value of the mortgage asset and the earnings on the MBS are paid from the regular interest and principal payment by the homeowners on their mortgage loans. Shadow banks have been in the fore of late especially because of their ability to securitize mortgages.

Why is shadow banking a concern around the world?

Shadow banking is touted as one of the biggest threats to the global economy. But isn’t it good enough if banking ancillary services are offered by institutions outside the banking industry? Doesn’t it create more competition among the banks and improves the quality of services as a whole?

Actually the potential point of concern here is not provision of banking facilities alone but provision of credit. If a non-banking entity, say Amazon, tomorrow comes up and helps people to manage their funds and assets, it would be welcomed rather than being questioned. The problem with shadow banking is the lending exercise they engage in. This is primarily because lending institutions are inherently fragile and play around maturity transformation to maximize profits. In this effort they tend to create enormous “maturity mismatches” and if at all there is a run on the institution they fall short of liquidity. Having said that, here is where the problem starts – traditional banking system is highly regulated by the central bank which is a watchdog to keep the banks within their safe lending limits. So, the capital adequacy of a bank is upheld. In addition to this, conventional banks are also backed by the government which acts as a safety net in case the banking system collapses. Both of the above mentioned points that help the traditional banks gain stability and credibility are elusive to the shadow banking system which is largely unregulated and not backed by any sovereign fund. This makes the SBS a trifle times more vulnerable and prone to market sentiments. SBS also got itself into bad light due to its engagement in lending using financial instruments that are called Off Balance Sheet (OBS) vehicles in financial parlance. These loans have no mention in the books of the institution which makes them very difficult to track and assess. OBS vehicles are typically considered to be separate from the banks but in practice are dependent on them.

How did the Shadow Banking System achieve its present size and avatar?

The birth of Shadow Banking system can primarily be attributed to the wariness of the scheduled commercial banks to lend money to small and medium scale businesses. The banks, beaten and battered, still coping with the bruises of the financial crisis are on the back foot and tend to retrench their expenses. Post crisis the banks have also been, rightly so, forced upon by more regulations which makes granting loans a lot more regulated activity now.

A typical supporting example is that of Republic of China. In China unlike other countries where market parameters play a vital role in setting the interest rate, it is the government that pins the interest rates for commercial lending. The government also imposes limits on loans and deposits that the banks can offer. The objective behind these regulative norms is to guarantee risk free profits for the banks. But, this leaves no incentive for the banks to remain competitive in the market by offering attractive lending rates to the customers. The result is focussed lending only to the state owned enterprises, which have near zero chances of default and are always backed by the government. Small and medium scale enterprises are thus left out of the official financial system and have no scope of borrowing money from the banks that are part of this farce system. As a result, SMEs look up to non-bank entities for credit which spawns the growth of institutions that engage in credit lending at high interest rate and take advantage of the situation. This constitutes the web of non-bank entities that make up the SBS. The Diplomat reports that China has grown to be the epicentre of ‘covert banking’ in recent times and shadow banking in China has grown by a startling 40% last year. Apparently, China is one country where shadow banking operations have grown at a rate more than formal banking operations have! JP Morgan pegs the size of the Chinese shadow banking operations to close to 46-50 trillion Yuan or $7.5-8 trillion which is about 30% of their total bank assets.

The authorities around the world are concerned about the shadow banking activities that have seen a manifold increase in the recent past - so much so, that shadow banking operations have affected the traditional financial sector and also the economy in general. Economists are examining more and more data closely to find the hidden vulnerabilities in this system and devise a solution for it. The most important step being taken by the authorities is to bring the area of operation of shadow banks under their purview so that the sector can be regulated and overseen thoroughly. One thing is for sure, shutting down shadow bank operations abruptly is out of question now; the way out lies in exercising greater control and expanding the scope of regulation in the financial market across all domains and sectors.

Pseudonym : h!v